Summary: The Dollar rebounded against its rivals boosted by rising US treasury yields in an otherwise featureless (data-wise) Monday. Ahead of key US treasury auctions this week, the benchmark 10-year yield climbed to one-month highs at 0.71% (0.68% yesterday). Against the Japanese Yen, the US Dollar soared the highest, up 1.02% to 107.65 (106.68). Risk currencies which have rallied since Thursday, stumbled led by the Australian Dollar, down 0.51% against the Greenback to 0.6490 (0.6532). The USD/CAD pair soared 0.74% to 1.4015 (1.3935) after Brent Crude Oil prices slid 3.2%. Sterling retreated against the Dollar to 1.2335 (1.2405) as British Prime Minister Boris Johnson spoke to his country Sunday on how to get the economy back to work. Johnson encouraged workers to return to work but also urged people to stay at home if possible, which was confusing to many. Johnson will give more details today. The Euro dipped 0.21% to 1.0815 from 1.0840 on the overall bid US Dollar. Against the Asian and EM currencies, the Greenback advanced. USD/SGD rallied to 1.4175 from 1.4125. Wall Street stocks finished with modest losses. The DOW slipped 0.72% to 24,215 (24,430). The S&P 500 was down 0.3% to 2,927 from 2,940 yesterday. Global treasury yields climbed, taking the lead from their US counterpart. Germany’s 10-year Bund yield finished at -0.52% from -0.53% yesterday. Japanese ten-year JGB yields were unchanged at 0.01%.

Yesterday’s data calendar was light. New Zealand’s ANZ Business Confidence Index was at -45.6 in April from March’s-66.6. Italy’s Industrial Production slumped to -28.4%, underwhelming expectations at -20.0%.

On the Lookout: Economic data releases pick up today. Fed speak picks up today with FOMC Members Patrick Harker (Fed President – Philadelphia) and Federal Reserve Governor and Vice-Chair Randal Quarles speaking at separate occasions. Cleveland President and FOMC member Loretta Mester speaks early tomorrow morning (Wednesday, 7 am Sydney). Input from the Federal Reserve speakers will impact the Dollar this week.

The current state of US-China relations is also a key potential issue, and any rise in tensions will impact risk appetite and the US Dollar.

Australia kicks off with its National Australia Bank Business Confidence Index. Japan reports on its Leading Indicators. Chinese CPI and PPI data follow. Also due today (no specific time given) is China’s Foreign Direct Investment (April). No Euro area reports are scheduled for release today. Australia’s Budget Release is due tonight (no specific time). US reports follow with its Headline and Core CPI data.

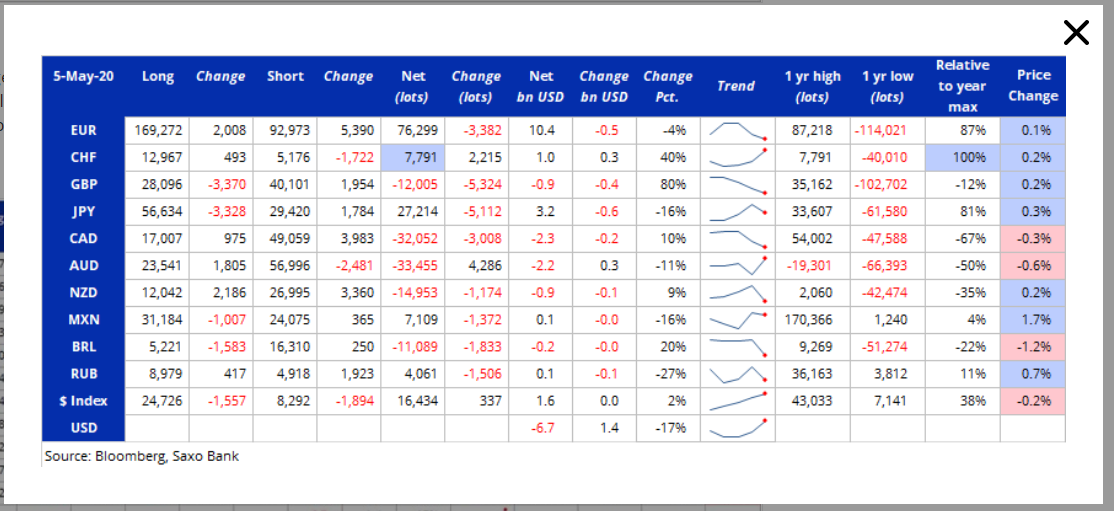

Trading Perspective: Amidst the rebound in US bond yields which has been a pillar of support for the Dollar, the latest Commitment of Traders report (week ended May 5) saw speculative USD shorts reduced for the second week in a row. Saxo Bank reported that speculative Dollar shorts were reduced by 17% to a total of -USD 6.7 billion. The Greenback was bought against the Euro, Yen, to reduce shorts. Against the Pound, and Canadian Dollar the Dollar was also bought, but for the purpose of adding shorts. The Greenback was sold against the Aussie to reduce shorts.

Given the economic reports being released this week, input from the various Fed speakers, Covid-19 flare-ups amidst a return to work in many countries, current state of US-China relations and market positioning, FX could be in for high volatility. Happy days.