Summary: FX markets were mostly uninterested, trading within recent ranges to closed little changed on Friday. On balance, the US Dollar was modestly lower against most of its rivals. Equities rallied in Europe and the US after earlier declines in China and other Asian markets. The rally in risk assets were powered by last week’s rise in China’s stock market to highs not seen since 2018, as well as growing expectations of more official global policy support. Meantime the spike in new coronavirus cases in the US and other global hotspots continued unabated. US President Donald Trump donned a mask for the first time since the pandemic began, yielding to pressure from the World Health Organisation urging countries to step up control measures. Currency markets were content to trade in familiar ranges with US Dollar bears taking the initiative. The Dollar broke its support against the Yen at 107.00, falling to 106.636 before settling at 106.90 and 107.22 Friday morning. The Euro rallied to 1.1307 (1.1282 Friday) on better-than-expected French and Italian Industrial Production reports. Sterling extended its gains to 1.2640 from 1.2605 on Friday, hitting an overnight peak at 1.26642. The Australian Dollar failed to take advantage of the overall weaker US Dollar, finishing modestly lower to 0.6955 from 0.6962. Yesterday the State of Victoria added 273 new Covid-19 cases while fears that a second wave has hit Sydney rose on growing new infections from a pub in the city’s southwest. The Kiwi (New Zealand Dollar) up a touch to 0.6577 (0.6568 Friday). EM Currencies finished mixed to mildly higher against the Greenback.

Wall Street stocks rallied with the DOW climbing 1.56% to 26,112 (25,705) while the S&P 500 added 1.17% to 3,190 (3,155 Friday). US bond yields rose with the key 10-year rate closing at 0.64% (0.61%). Germany’s 10-year Bund Yield was last at -0.47% from -0.46% Friday.

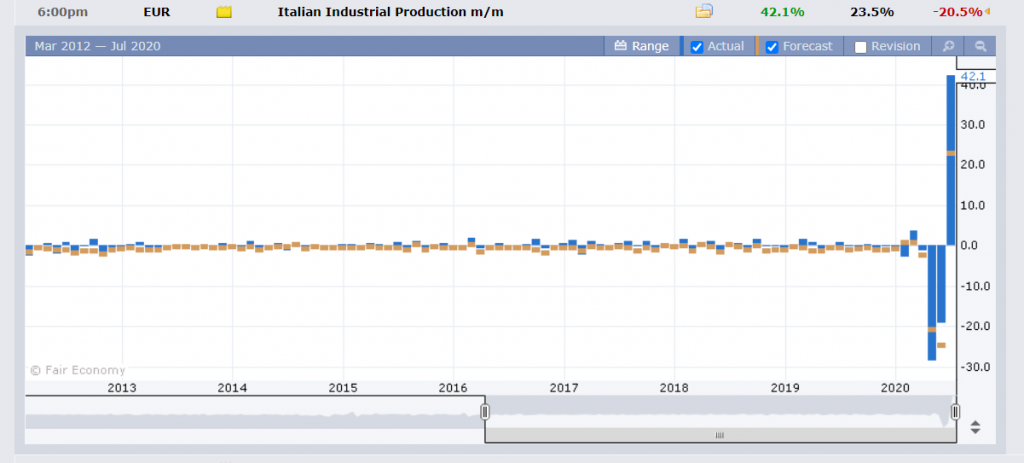

Data released on Friday saw French Industrial Production climb 19.6% in June, beating expectations of a 15.2% rise. Italy’s Industrial Production rose 42.1%, beating median forecasts at 23.5% and a previous contraction at -20.5%. Canada’s Employment Change saw 952,900 Jobs created, bettering forecasts of a 700,000 rise. The Jobless rate though rose to 12.3%, worse than the 12.0% forecast. US Headline PPI fell in June to -0.2% against expectations of 0.4% while Core PPI was lower to -0.3%, against forecasts at 0.1%.

On the Lookout: Expect a slow start to Asia today with the focus on China’s stock market and the growing spike in new global coronavirus cases. Data releases today are light ahead of a big week of economic reports beginning tomorrow. The Earnings Season begins following the second quarter’s dramatic rebound in global financial markets. Tomorrow will see Chinese Foreign Direct Investment, Industrial Production, and Trade data. Further on in the week, the Bank of Japan policy meeting and rate announcement is on Wednesday. The ECB has its rate policy meeting and Monetary Policy Statement on Thursday.

Earlier today, New Zealand released its Food Price Inflation for June, up 0.5% from May’s -0.8%. The Kiwi did not budge. Japan reports on its Tertiary Industrial Account data. Europe see Germany’s WPI (Wholesale Price Index) for June. Bank of England Governor Bailey is due to speak at a Webinar on LIBOR (London Interbank Rate) as a webinar hosted by the Bank of England and US Federal Reserve. Later in the day, US New York Fed President and FOMC Member John Williams also speaks at the LIBOR webinar.

Trading Perspective: Expect Asia to extend the FX range trading with the Dollar under pressure first up. However, any further news reports regarding fresh spikes of Covid-19 cases in the US and elsewhere will see safe-haven support for the Greenback to drive the US currency higher. Markets will keep their ammunition dry ahead of this week’s economic data deluge and events (BOJ and ECB rate policy meetings and announcements). Traders will also monitor official efforts to support policy, which many believe is forthcoming. This will keep the Dollar under pressure.