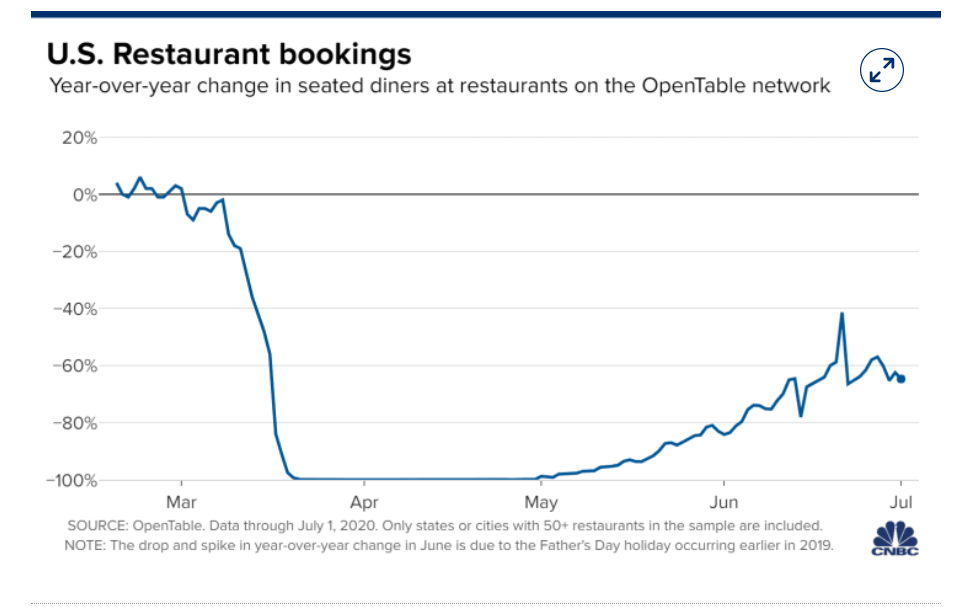

Summary: Currencies were confined to narrow ranges on Friday with US Forex markets closed in observance of America’s Independence Day. The Dollar Index (USD/DXY) a favoured gauge of the Greenback against a basket of 6 major currencies, eased to 97.152 from 97.220. Meantime the coronavirus resurgence in the United States continued unabated. Rising cases in several US states dampened the positive effects if a strong US payrolls report released Thursday. Florida and Texas both hit record highs for new coronavirus cases. Rising Covid-19 cases have started to affect businesses like restaurants where bookings appeared to be recovering since they fell to zero in late March and April. However, according to data from reservation service Open Table, there have been recent declines in restaurant bookings due to the rising virus cases. The Euro was little changed at 1.1248 from 1.1240 despite comments from ECB Head Christine Lagarde that the ECB will need to keep its monetary policy exceptionally loose. Sterling closed a touch lower to 1.2482 (1.2468). The European Union and the Britain committed to another round of Brexit talks this coming weekend. In quiet trade, the Australian Dollar rose to 0.6940 from 0.6925 even as new Covid-19 cases in the second most populous state of Victoria continued to climb over the weekend. Against the Yen, the Dollar finished dead flat at 107.50 (107.50). The US Dollar edged lower against the Canadian Loonie to 1.3550 from 1.3570 Friday. European stocks and US futures slipped. US S&P 500 futures were 0.33% lower to 3,125 from 3,135. DOW Futures declined 0.43% to 25,750 from 25,855 Friday. US Treasury markets were closed on Friday while global bond yields elsewhere were lower. Germany’s 10-year Bund yield dipped 3 basis points to -0.43%. Japan’s 10-year JGB rate was last at 0.02% (0.03% Friday).

Forex Data released Friday saw Australia’s June Retail Sales climb 16.9%, beating forecasts at 16.3%. China’s Caixin Services PMI rose in June to 58.4 from the previous month’s 55.0 beating expectations of 53.0. Euro area Services PMI’s were mostly up, Spain rose to 50.2, bettering forecasts at 46.0 while Italy’s Services PMI rose to 46.4 from 28.9 but missed forecasts at 46.9. French Services PMI climbed to 50.7, beating expectations of 50.3. The Eurozone’s Final Services PMI rose to 48.3 from 47.3, bettering forecasts at 47.3. Germany’s Final Manufacturing PMI rose to 47.3 from a previous 45.8, beating expectations of 45.8. The UK’s Final Services PMI virtually matched forecasts at 47.1 (47.0).

On the Lookout: Expect a slow start in Asia today with a light economic calendar today. New Zealand kicks off with its ANZ Commodity Price Index for June. Australia’s University of Melbourne releases its June TD Securities Inflation report followed by ANZ Job Ads for June. European reports start with Germany’s June Factor Orders. Spain follows with its Industrial Output data. The Eurozone Sentix Investor Confidence Survey and Eurozone Retail Sales follows next. The UK releases its Markit Construction PMI for June. The US returns with its June Markit Services and Composite PMI’s, and ISM Non-Manufacturing PMI. Finally, Canada releases its Bank of Canada Business Outlook Survey. Looking ahead to this week, the main events will be the RBA’s policy meeting and rate announcement tomorrow, as well as Germany’s Industrial Production. Wednesday sees the European Union’s Economic Forecasts. Traders will look to Thursday US Jobless Claims which last week rose more than economists expected. There are no forecasts for the number this week so far.

Trading Perspective: Traders will keep their focus on the rising pandemic figures in the US, which have exceeded 50,000 per day every day this month. Tensions between the US and China on another front are building which will also keep the market’s attention. China plans to hold military exercises in Asia’s South China sea, one of the regions hottest spots. While the world is busy combating Covid-19, China has been fortifying its islands where they have runways and dozens of hangars for fighter aircraft, as well as anti-ship cruise missiles and missile defenses. The Wall Street Journal reported this weekend that the US is sending two aircraft carriers to the region with the US Navy set to hold some of the largest exercises in recent years in the South China sea.

While the Dollar ended on a weaker note on Friday in forex market , the safe-haven attraction will give the Greenback support.