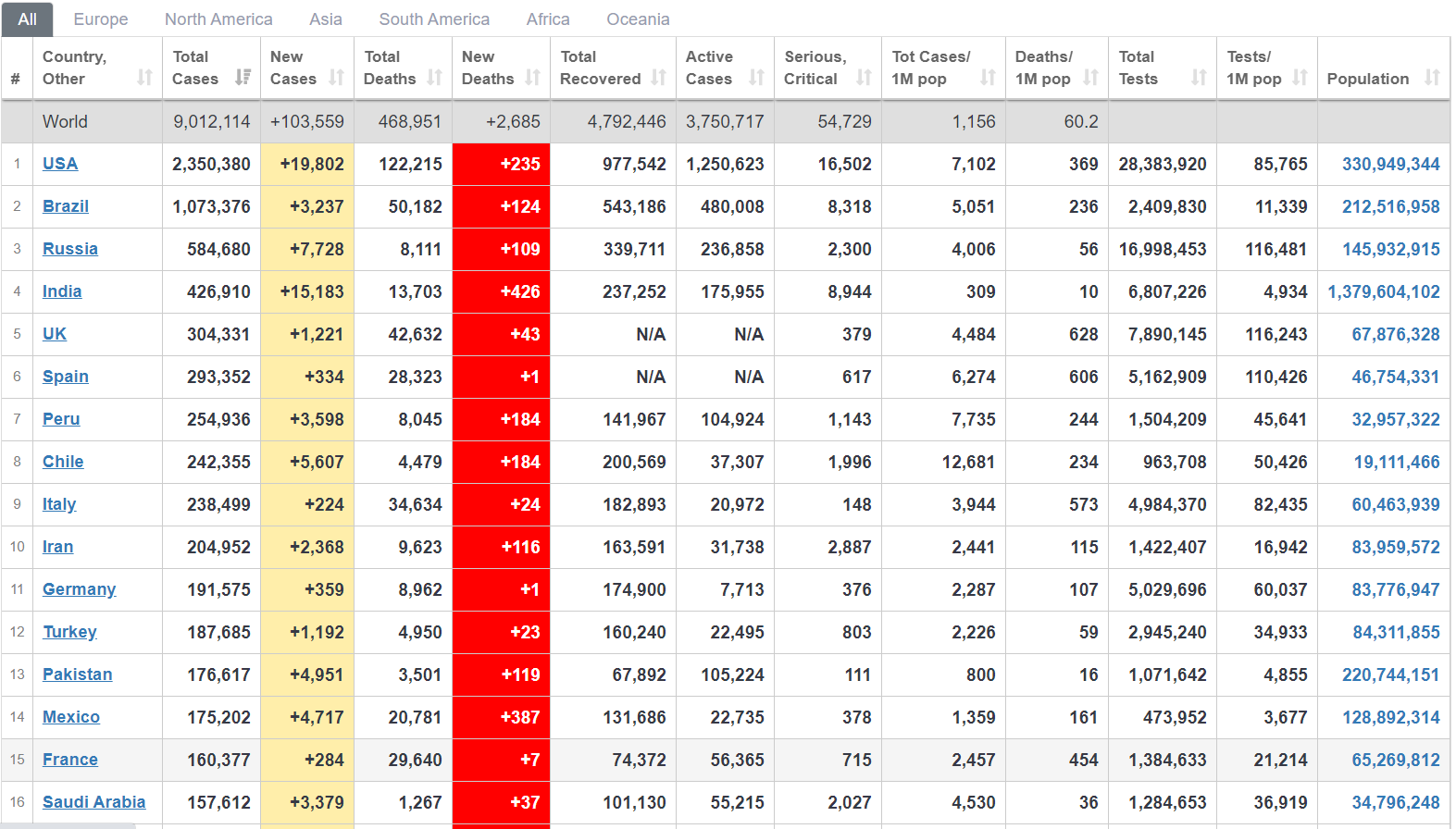

Summary: There was no let-down in the recent spike in global Covid-19 cases and deaths which kept markets in risk-off mode. The Dollar Index (USD/DXY), a favoured gauge of the Greenback’s value against a basket of 6 major currencies rose 0.25% to 97.663 (97.453 Friday). According to data compiled by Johns Hopkins University, the US reported 30,000 new coronavirus cases over the weekend, the highest daily total since May 1. The Johns Hopkins worldometer saw India’s Covid-19 death toll spike to 426 on Saturday. For the week, USD/DXY was up 0.95%. Sterling slumped 0.85% to 1.2350 (1.2430) after Britain’s Public Sector Net Borrowing (debt) rose more than expected. The Euro was weaker, down 0.35% to 1.1209 from 1.1240. At the European Union’s summit, ECB head Christine Lagarde told EU leaders that their economy was in a “dramatic fall” and called for the bloc to act to spearhead a revival. The Australian Dollar led risk currencies lower, down 0.39% to 0.6854 (0.6884 Friday). In early Monday morning Asia, AUD/USD slipped further to 0.6822 after China suspended its meat imports from Tyson Foods, a US chicken, beef, and pork producer and exporter. China’s backed media Global Times cited Covid-19 infections linked to meat plants in the US as well as trade tensions between the two nations. The USD/JPY pair was marginally lower to 106.90 from 107.00. Against the Canadian Loonie, the Greenback climbed to 1.3620 in early Asia from its NY close at 1.3600 and 1.3565 opening on Friday. Wall Street stocks retreated. The DOW was 1.49% lower to 25,650 (26,075) while the SP 500 dropped 1.25% to 3,072 from 3,112.

Data released on Friday saw Japan’s National Core CPI drop to -0.2% against forecasts at -0.1%. Australia’s Retail Sales in May rose 16.3% from April’s -17.7% which was expected. Germany’s PPI dipped to -0.4%, lower than expectations of -0.3%. UK Public Sector Net Borrowing climbed to GBP 54.4 billion, against forecasts at GBP 49.3 billion. Britain’s May Retail Sales rose 12% after falling by 18% in April. Canada’s Core Retail Sales in May slumped -22.0% underwhelming forecasts at -12.7% and Aprils upwardly revised -0.2% (from -0.4%.

On the Lookout: Today’s economic data calendar is light, and traders will continue to focus on the second wave of coronavirus new cases and deaths as well as the China-US trade tensions.

RBA Governor Philip Lowe is due to speak this morning (9 am Sydney) at a panel discussion in the Australian National University Crawford Leadership forum on Covid-19 and the global economy.

New Zealand reports it Credit Card Spending (year on year). China releases its Conference Board’s Leading Index (May). The UK kick off European data with its CBI (Confederation of British Industry) Industrial Order Expectations. Germany’s Bundesbank its Monthly Report. The Eurozone follows next with its Consumer Confidence data. Finally, the US releases its Existing Home Sales report.

The week ahead sees Global Flash and Services PMI’s released tomorrow. The RBNZ policy meeting and rate announcement is scheduled Wednesday. US Headline and Core Durable Goods Orders data is released on Thursday.

Trading Perspective: Risk aversion will continue to support the Dollar on dips, dominating Asian trade. The spotlight will be on the rising number of new daily cases and deaths in the US and other current hotspots like India, Brazil, and Mexico in the developing nations, as well as Germany, Japan, and Beijing. Ongoing China-US trade tensions will also occupy traders today.