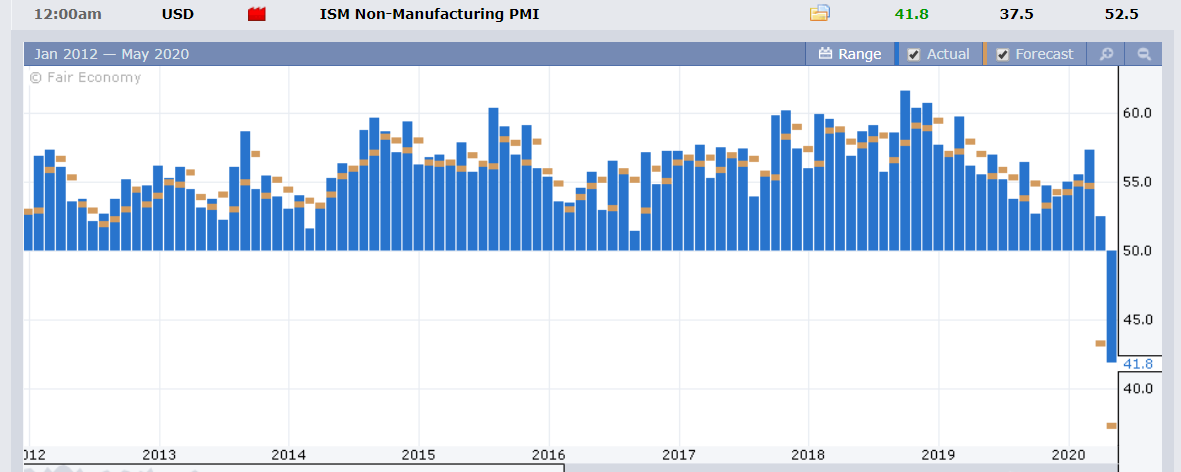

Summary: The Euro slumped 0.61% to 1.0837 (1.0902) after Germany’s Constitutional Court ruled that the Bundesbank should stop buying government bonds if the ECB cannot prove that the purchases are needed. This propelled the Dollar Index (USD/DXY), a gauge of the Greenback’s value against a basket of foreign currencies, in which the Euro takes 60% of the weight, up 0.37% to 99.848 (99.54). The Australian Dollar lifted 0.15% to 0.6435 (0.6423) after the RBA kept its interest rates and policy unchanged. While the move was widely expected, policymakers did not signal an immediate need for additional easing. Against the Canadian Loonie, the US Dollar dipped to 1.4053 (1.4095) after oil prices rallied. WTI (West Texas Intermediate) up 22.3% (US$26.25). Sterling closed little changed at 1.2437 (1.2440). Trading was light due to the Japanese and Chinese Golden Week holidays. USD/JPY finished at 106.54 (106.72 yesterday). US bond yields climbed. The benchmark 10-year treasury rate was at 0.63% (0.61% yesterday). Germany’s 10-year Bund yield finished at -0.57% from -0.59%. Wall Street stocks slipped off their highs, still ending in positive territory. The DOW was 0.13%% higher in late New York at 23,867 (23,734) while the S&P 500 added 1.05% to 2,866 (2,836). Investor optimism rose as some US states ease restrictions to spark their economies. US Service Sector activity (ISM Non-Manufacturing PMI) bettered market forecasts of 38 with a 41.8 print, down from the previous 52.5. Other data released yesterday saw Eurozone PPI fall to -1.5%, lower than expectations of -1.2% and a previous -0.7%. The US Trade deficit rose to -USD 44.4 billion from -39.9 billion, underwhelming expectations of -USD 41.0 billion.

On the Lookout: It’s all about the data ahead which culminates in Friday’s US Payrolls report. Earlier today, New Zealand released its Q1 Employment report, which rose to 0.7%, beating expectations of -0.2%. New Zealand’s Unemployment rate dipped to 4.2%, beating forecasts at 4.4%. The Kiwi which closed at 0.6055, popped to 0.6070 before dropping to 0.6060 on the report. The data covered the period before New Zealand went into its lockdown.

Other data scheduled for release today begin with Australia’s Retail Sales for April which could move the currency. Retail Sales are forecast to slump to -10% from March’s -1.4%.

Euro area reports see Germany’s Factory Orders. Services PMI’s from Italy, Spain, France, Germany, and the Eurozone follow. The Eurozone also releases its Retail Sales (April). The European Union releases its Economic Forecast which will keenly be focussed on. The UK reports on its Construction PMI. The final report for today is the US ADP Non-Farm Employment Change. Expectations in the Private Employment sector are forecast by economists to drop to -20,000K versus the previous month’s -27K. Again, more prospects for fireworks following the release of this number.

Trading Perspective: While trading conditions remained thin due to the Japanese and Chinese holidays, there were some volatile moves within the ranges that were established yesterday. Today the US Dollar faces a test with the release of the upcoming data. While the correlation between the US Dollar and equity markets is positive now, much of that is the result of thin markets. This could change on a sixpence. Market positioning has also been a factor. We highlighted yesterday that while net speculative Euro long bets were trimmed, the total was still near 2018 highs. Against the Australian Dollar, speculative short Aussie bets saw a slight increase. Expect these factors to continue to be an influence in FX.