Summary: The Dollar finished the week lower against its rivals in dull trading on Friday even as the total death toll in the US topped 140,000. Daily new cases continued to rise in 43 out of 50 states over the past two weeks, according to a Reuters tally. More states have been forced to put a halt to, or roll-back their reopening measures. Meantime, across the Atlantic, European Union leaders had to extend their summit by one more day as they failed to agree on a massive stimulus fund to revive their Covid-19 struck economies. At the close of trading in New York, the Euro was up against the Dollar by 0.23% to 1.1427. Against the Japanese Yen, the Greenback slid to 107.03 from 107.35. Sterling failed to take advantage of the weaker Dollar, finishing little-changed at 1.2570 (1.2580) with traders still concerned that the UK’s ongoing reopening will result in a second wave of coronavirus infections. The Australian Dollar managed a 0.15% gain to 0.6995 despite a continuing rise in Covid-19 community transmissions in New South Wales, the most populous state. Yesterday the state reported 18 new cases. Victoria, Australia’s coronavirus epicentre, recorded 363 new cases and 3 deaths. Asian currencies led the rally against the Greenback, with the USD/CNH (Dollar-Offshore Chinese Yuan) maintain near March lows at 6.9900. The USD/ZAR (US Dollar-South African Rand) closed 0.70% lower to 16.6800. Wall Street stocks were mixed with the DOW down 0.18% to 26,665. The S&P 500 gained 0.54% to 3,225. Optimism for an eventual coronavirus vaccine and hopes for more stimulus measures to power a post-pandemic economic recovery continued to drive equities higher. The G20 virtual meeting over the weekend saw member nations pledge to use “all available policy tools” to fight the coronavirus outbreak.

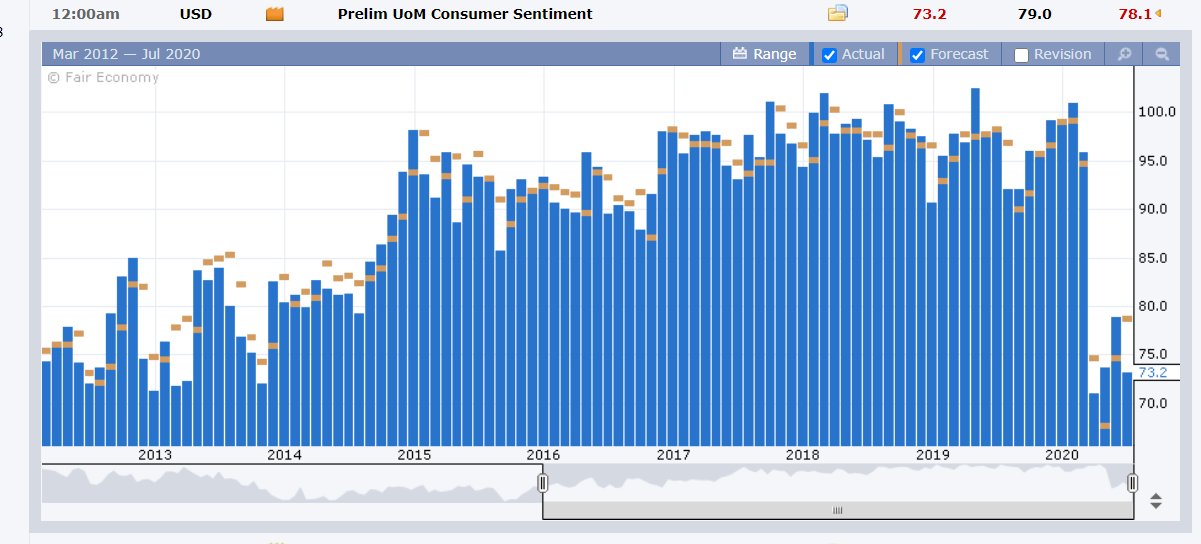

Data released on Friday saw Canada’s Wholesale Sales in June slump to 5.7%, missing forecasts at 7.4%. US Building Permits underwhelmed forecasts at 1.24 million against expectations of 1.30 million. The University of Michigan Preliminary Consumer Sentiment Index in July fell to 73.2 from a downwardly revised 78.1 in June.

On the Lookout: After summer-like doldrums hit FX most of last week with tight trading ranges developing, the US Dollar was still weaker overall at the end of the week. Economic data in the week ahead is considerably light as we head into the middle of the northern hemisphere summer season. Markets will look to another round of stimulus measures from various governments, led by the US as the resurgence of the coronavirus continues to grow at alarming rates in many areas around the globe. Monday’s reports kick off with Japan’s Trade Balance and the BOJ’s latest meeting minutes release. European data starts with Germany’s PPI (June) as well as the Bundesbank report. The Eurozone releases its Current Account data. The US has no major economic releases scheduled. The week ahead sees The RBA’s meeting minutes release on Tuesday, Australian Retail Sales (Wednesday). On Thursday, Euro area, Eurozone, UK and US Manufacturing PMI’s are scheduled for release.

Trading Perspective: There may be some gaps this morning in early Asia with the Dollar clawing back some of its losses following the weekend news. The EU should have had a decision by now on the massive stimulus fund. The delay will weigh on the shared currency and see a short-term bounce on the US Dollar. Market sentiment has been leaning against the Greenback as Europe’s success in dealing with Covid-19 contrasts starkly with that of the US. The economies will reflect this as markets digest upcoming data.

Meantime the virus outbreak and efforts to contain it seems to have taken a turn for the worse as growing infections continue to surge in various pockets around the globe. The US Dollar may benefit from it’s safe-haven status which has grown since the start of the pandemic. Could be an interesting start for this week today and the catalyst to see some volatility return to FX.