Summary: The US Dollar, Wall Street stocks and bond yields eased in high volatile trade ahead of the Federal Reserve’s June meeting and outcome (4 am, Sydney, 11 June; 2 pm NY, 10 June). The Fed is expected to release its economic and interest rate forecasts, which it did not do at its March meeting at the height of the crisis. Most economists are expecting US policymakers to remain on the side of being accommodative. Which saw the Dollar finish mostly lower after initially spiking higher on profit-taking in high volatile trade. Risk-on went out the window and volatility entered. The Euro bounced back from an overnight low at 1.1241 to finish at 1.1336 in late New York. The Australian Dollar ended its 8-day winning streak, plunging initially to 0.68985 overnight lows from its 0.7020 open yesterday, eventually settling at 0.6962. Against the Japanese Yen, the Dollar dropped anew to 107.75 (108.43 yesterday). Sterling had a see-saw session between 1.2618 and 1.2756, settling at 1.2730 in late NY trade, little changed from 1.2725 yesterday. The USD/CAD pair was 0.3% higher to 1.3415 (1.3378). The Kiwi ended at 0.6515 in NY from 0.6560 yesterday. Against the Offshore Chinese Yuan, the Dollar (USD/CNH) climbed back to 7.0790 from 7.0575.

Wall Street stocks eased. The DOW closed at 27,280 (27,545). The S&P 500 was at 3,207 (3,229).

The benchmark US 10-year Treasury yield dropped 5 basis points to 0.83%. Germany’s 10-year Bund yield was up one basis point to-0.31%. Japanese 10-year JGBs yielded 0.01% from 0.04%.

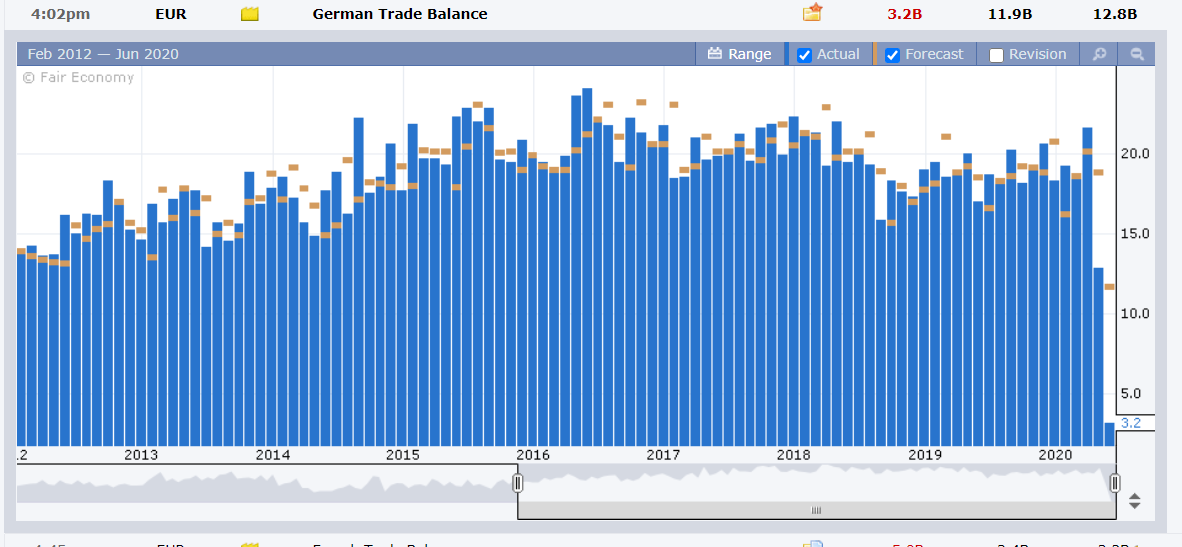

Germany’s Trade Surplus slumped to +EUR 3.2 billion in May from April’s +EUR 12.8 billion, and missing forecasts at +EUR 11.9 billion. US JOLTS Job Openings fell to 5.05 million, missing expectations at 5.75 million and a previous downwardly revised 6.01 million.

On the Lookout: All eyes on the Fed today. Most economists think that the US central bank will keep leaning on the side of being accommodative. The FOMC is not expected to change interest rates or increase Quantitative Easing (QE). The spotlight will be on the Fed’s interest rate (dot plot) and economic projections. Rather than risk a “taper tantrum”, most traders expect the Fed to stay dovish. Any diversion from this leaning would see the Greenback rebound strongly. Federal Reserve Chair Jerome Powell follows the meeting (30 minutes later) with his press conference. Powell could be less downbeat instead pointing to recent signs of a recovery.

Markets will also focus on the other economic data releases today. New Zealand kicks off with its Q1 Manufacturing Sales report. Australia reports its Westpac Consumer Sentiment. Japanese Core Machinery Orders, and PPI follow. China releases its CPI and PPI data. The Euro area sees French Industrial Production. Finally, the US reports on its Headline and Core CPI before the Fed meeting outcome, statement, economic projections and FOMC press conference.

Trading Perspective: The Dollar initially rebounded strongly against its rivals as traders took profits and adjusted positions. In choppy trade, the Greenback surrendered it’s advance against the currencies on expectations of bearish interest rate and economic projections from the US Federal Reserve at the conclusion of its meeting today. Fed Chair Jerome Powell will likely be cautiously optimistic in his assessment of the economy.

Markets have ignored US-China tensions which featured heavily last week. US Secretary of State Mike Pompeo in his latest press conference criticised British bank HSBC for backing China’s plan to impose new security legislation on Hong Kong. This is a negative for risk-on and could add to volatility ahead of the Fed meeting.

FX sentiment towards the Greenback remains decidedly bearish. The risk is for further US Dollar upside correction.