Summary: The Dollar Index (USD/DXY), a popular gauge of the Greenback’s value against a basket of 6 major currencies fell 0.56% to 99.558 (100.183) after the Federal Reserve announced it provide USD 2.3 trillion in loans to businesses to support the economy. US Initial Jobless Claims climbed to 6.606 million in the week ended March 3, more than economist’s expectations of 5 million. Best performing currency went to the Australian Dollar, for the second day running, this time surging 1.65% to 0.6340 (0.6232). The Euro advanced 0.65% to 1.0927 (1.0855) against the broadly-based weaker US Dollar. Sterling rose 0.53% to 1.2460 (1.2380), aided by the news that UK PM Boris Johnson has left ICU. The US Dollar dropped 0.8% against the Canadian Loonie to 1.3980 (1.4020) despite a fall in Brent Crude Oil prices and a dismal Employment Report. USD/JPY dipped to 108.50 from 108.90 on lower US bond yields. Emerging Market currencies extended their rallies against the Greenback. Against the South African Rand, the Dollar slid to 18.0300 from 18.20 yesterday.

Wall Street stocks rose. The DOW added 1.7% to 23,790 (23,080) while the S&P 500 rose 1.8% to 2,790 (2,750). The benchmark US 10-Year bond yield eased to 0.72% from 0.77% yesterday. Germany’s 10-year Bund yield was 5 basis points lower to -0.36%.

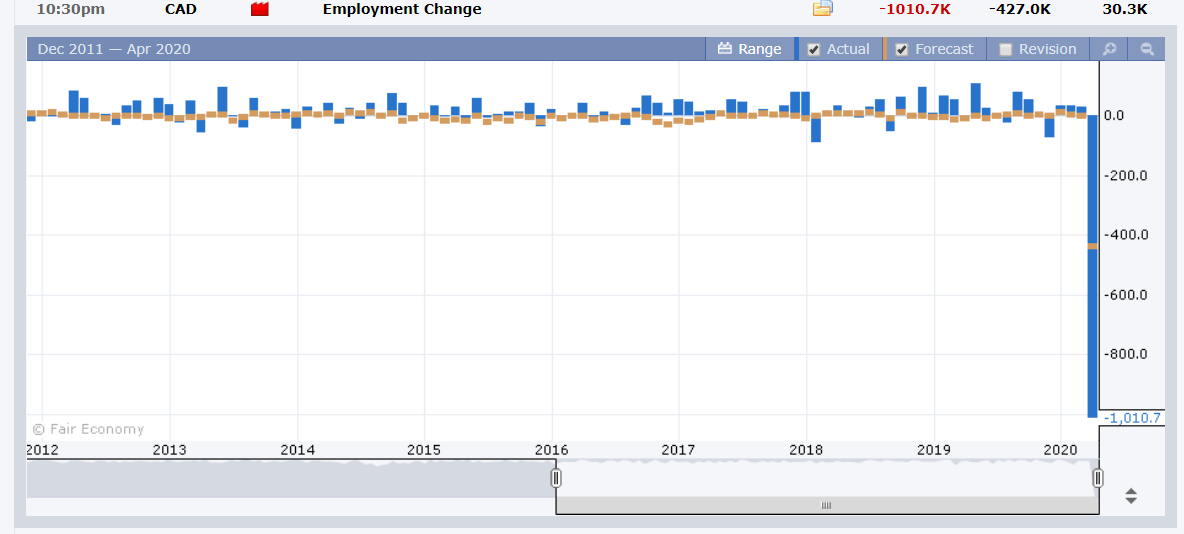

UK Construction Output underwhelmed to -1.7% against forecasts of +0.3%. Britain’s Trade Deficit widened to -GBP 11.58 billion from -GBP 3.7 billion. Italian Industrial Production beat forecasts, rising to -1.2% against -1.6%. Canada’s Employment plunged by 1.01 million workers, more than twice the total job losses during the 2008/2009 global financial crisis and much worse than forecasts of a 427,000 loss. The Unemployment rate in March jumped to 7.8%, from 5.6%. US Core PPI rose to 0.2%, beating forecasts of 0.0%. Headline Producer Prices were at -0.2% against forecasts at -0.3%.

On the Lookout: Today FX trading will be thin with Australia, New Zealand, Switzerland, the UK and Canada closed in observance of Good Friday. On Monday, apart from those closed today, most of Europe will also be closed to observe Easter Monday.

The focus will be on the G20 meetings and the US CPI release (both today).

Other data releases today are Japan’s PPI and Bank Lending reports. China releases its Annual CPI and PPI data. Europe sees French Industrial Production before the US Headline and CPI numbers are released. Federal Reserve FOMC members Loretta Mester and Randal Quarles have speaking engagements.

Trading Perspective: The Dollar retreated on the back of the dismal US Jobless Claims and lower bond yields following the Fed’s announcement of direct loans to small and medium size companies. Jerome Powell, in a speech afterwards, said that the US central bank would continue to use all the tools at its disposal until the US economy begins to rebound fully from the harm caused by the Covid-19 breakout. This reduced the Dollar’s safe haven support, boosting risk currencies like the Aussie, Kiwi, Canadian Loonie as well as EMS.

While this is the case, speculative market positioning remains mostly short of US Dollars mainly against the Euro. Dollar shorts have also been established against the Yen, Sterling and Canadian Dollar to a lesser extent. Today begins the long Easter weekend where liquidity is at a premium and market positioning is a factor. Not a time for any strong opinions. Look to trade within established ranges.