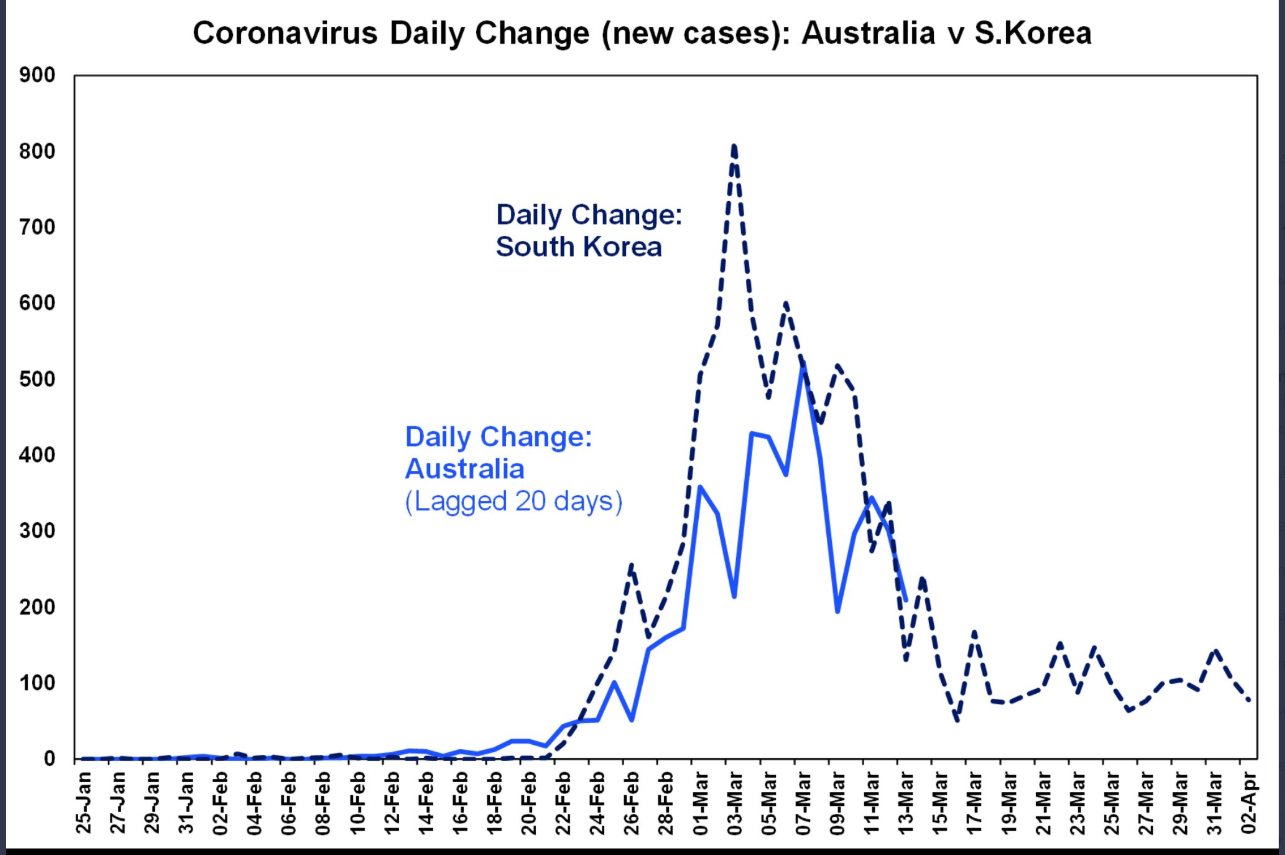

Summary: The Australian Dollar starred in the FX world despite a cut by ratings agency S&P on Australia’s sovereign outlook. Traders shrugged off the downgrade, preferring to focus on the RBA’s recent QE remarks as on the verge of tapering. AUD/USD rocketed to 0.62449 overnight and 3-week high after initially dropping to 0.61158 following the S&P ratings announcement. The Aussie Battler closed at 0.6235, up 1.23%. Australia’s coronavirus daily change appeared to be tapering, following that of South Korea. The FOMC meeting minutes revealed that the Fed would keep rates near zero until the country has weathered the coronavirus impact. The Euro extended its retreat, dipping to 1.0855 (1.0895) after European Union finance ministers failed to agree on further support measures for their economies. The Eurogroup meetings were suspended until later today (European time). Against the Yen the US Dollar advanced modestly to 108.90 from 108.75. Sterling was up 0.3% to 1.2370 from 1.2340. USD/CAD edged up to 1.4017 from 1.3997 despite higher oil prices. Wall Street stocks ended higher as the US appeared to be getting on top of the Covid-19 curve, with the possibility of more government stimulus measures. In late New York, the DOW was up 3.9% to 23,420 (22,550) while the S&P 500 gained 3.85% to 2,750 (2,647). The benchmark US 10-year treasury yield climbed 6 basis points to 0.77%. Other global bond yields were little changed.

There were limited data releases yesterday. Japan’s Core Machinery Orders (March) beat forecasts, climbing to +2.3% (-2.9%). Japanese Economic Watcher’s Sentiment Index dropped to 14.2, missing expectations of 22.2. Canada’s Housing Starts were up to 195,000, bettering expectations of 173,000 while the country’s Building Permits slumped to -7.3%, worse than the -4.0% forecast.

On the Lookout: Today is the last full trading day with many markets closed for the Good Friday observation tomorrow. Hence liquidity will be at a premium. The spotlight will continue to be on coronavirus developments and its impact on the global economy.

Data today sees Japanese Machine Tool Orders (March). European reports follow with Italy’s Industrial Production. The UK sees Construction Output, RICS House Price Balance, Manufacturing Production, and Goods Trade Balance.

The Eurogroup meeting of Eurozone finance ministers resumes today. OPEC meetings also start today (European time). Canada reports its Employment Change (March) and Unemployment rate. Traders will focus on the US Weekly Unemployment Claims, where median forecasts are between 5,000K and 5,250K from last week’s 6,648K. Anything outside of these forecasts could see some violent FX moves. US Headline and Core PPI, and Preliminary University of Michigan Consumer sentiment follows. Finally, Jerome Powell is scheduled to speak on the US economy to the Brookings Institution in Washington DC via satellite.

Trading Perspective: As we approach the Easter long weekend, the main thing to remember if, and when you trade is that liquidity is at a premium. This is not the time to have any strong views or fall in love with a view. Look for extremes, get in and out quickly and stay flexible. Take smaller bets (position size) so you can fine tune your stop loss and take profit levels. Otherwise, take time out to commemorate the events of the season. Another saying that many traders said in the day was “when in doubt, stay out.” Still holds for today. That said, there are some good levels to monitor in the currencies today.

Today’s main event will be the US Weekly Jobless Claims and Powell’s speech.